Does Momentum Trading really work?

Pic 1 – shows the ‘raw’ momentum approach (small caps) works in some years sporadically and needs to be switched (tilted) on/off frequently (However, a different rebalance frequency may yield different results admittedly)

Pic 2 – shows that my bespoke momentum signals (small caps) provide consistent outperformance in all market regimes

After one post I made on Linkedin concerning my momentum signals: I was asked by a skeptic why I thought Momentum trading works even though some studies (like the original one by Jegadesh/Titman) have shown the returns eventually can reverse. My response was that some studies look at Momentum returns (i) agnostic of the current point in the cycle (without testing performance in distinct macro regimes) and/or these studies (ii) use raw momentum scores and weightings instead of more sophisticated methods.

To prove these two points (and that my signals outperform): I decided to test the raw momentum approach vs my bespoke signals on a longer time period. In the test I do not allow shorts nor leverage and I compare the weekly rebalance performance with fees to a buy/hold strategy. The Momentum factor is thought by many to not do well in bear markets – my tests show this is the case for a ‘raw’ momentum approach that most Investment Funds use, but my bespoke signals show a different story – they provided bear market outperformance. Why? Because they set the ‘losers’ to low/zero weight.

Pic 3 (below) – Shows a more advanced proprietary model – which uses momentum and volatility and has only seen data before 2010, nonetheless is able to strongly outperform from 2010-2024 (small caps)

2024 Global Multi-Asset Performance

My 1st year part-time investing, and my Global Multi-Asset strategy returned 9.31% IRR. Just shy of the Hedge Fund Global Macro average (aurum.com) at 9.42% and beating JPM’s Global Macro Fund C at 8.85%.

Luckily, I was able to exit my mid corp Germany/UK positions at the right time – with no losses. Sadly, I haven’t had the heart to sell my ailing French CAC 40 position at a loss yet – definitely a lesson on anchoring bias. My Gov bond positions are being hammered by the current inflation story – but these have been completely offset thanks to Gold and USD strengthening. My FX ETF trade: long Yen short USD, was a huge lesson to not use these sorts of ETFs for FX exposure and to instead invest in the currency you want to be long in, because the FX ETF has no yield attached – but an investment does.

It’s crazy to think US/UK rates are almost back at levels we saw a few years ago at the start of the inflationary crisis. This time it’s due to the impact of Western Gov spending + Trump protectionism, but also diversification of Eastern Central Banks away from USD Treasuries and growing currency bilateralism/de-dollarisation. The US Treasury may essentially ‘need’ inflation to monetise and reduce Debt levels – weakening the reserves of other central banks. The inflation fear might be overplayed.

In the UK, steepening of the curve continues with 30 year rates at over 5.2%. German 10 year bunds currently at 2.5% – one wonders if the EU will eventually get itself together, re-read Draghi’s paper and start growing again? Also, wondering if it’s time to dip into Chinese stocks yet or if the political/macro risks are too great. Crypto should probably get a seat at the table, even if the allocation is only 1-2% – but which coin?

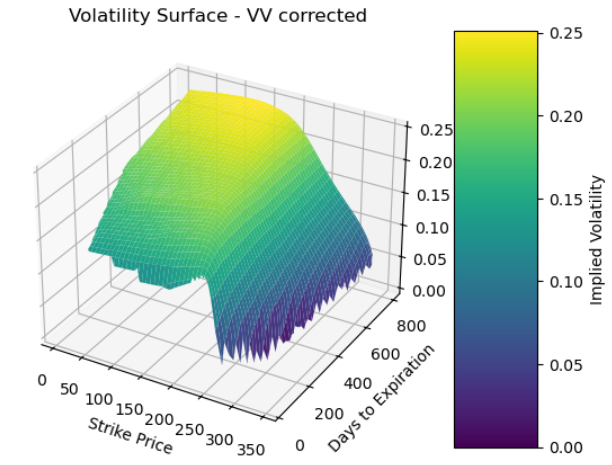

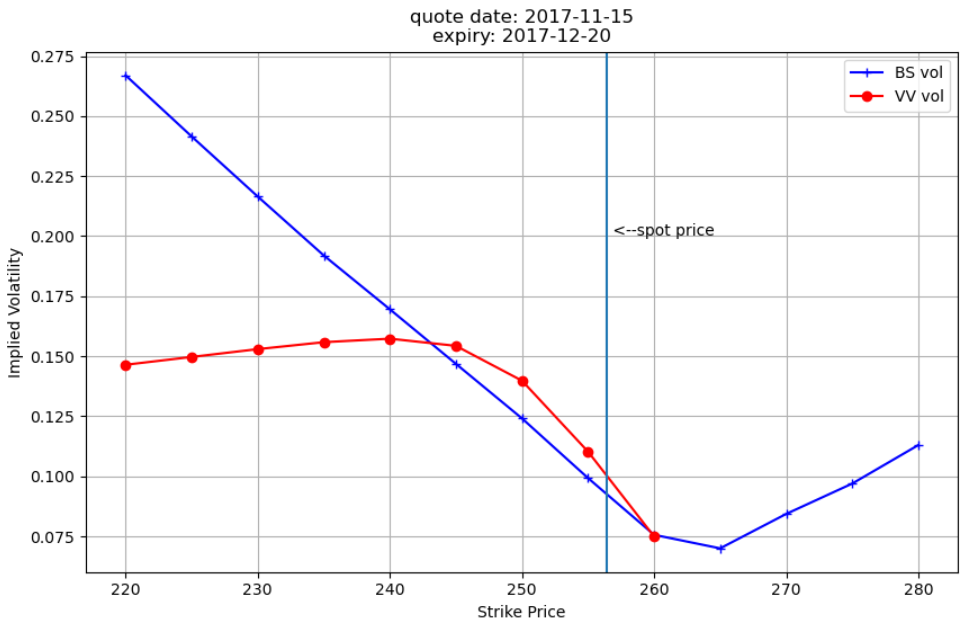

Some Options Research

Two images that show some options research, and how the Volga-Vanna correction (used a lot in FX options) can be used to get a more realistic value for volatility (vs the Black Scholes vol) – the application is towards option vol arbitrage, mainly on time to expiry, buying when vol is low and selling when it is high.